How to estimate costs for your health plan

It might be tempting to buy a health plan based with the lowest monthly premium, but if you do, you might be surprised at your costs at the end of the year.

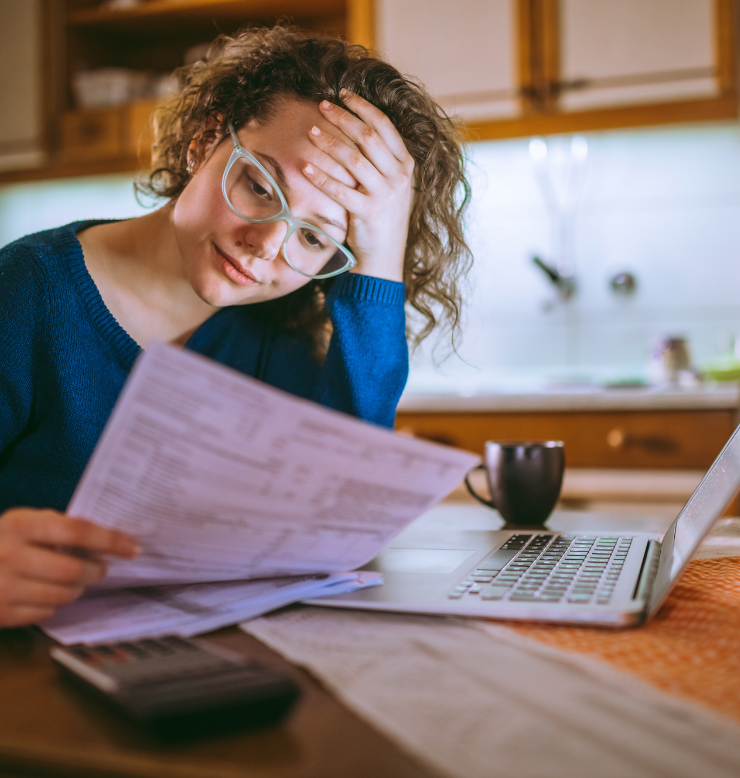

So, when you compare plan prices, it’s important to estimate your total yearly costs so you can find a plan that meets your needs and budget.

Consider what you might need to spend:

Consider what you might need to spend:

- The monthly premium, the bill you pay each month. Think of it as a fixed cost.

- Deductibles are what you must pay before your plan pays for anything except free preventive services or other no-cost services your plan might offer.

- Once you meet your deductible, you still have costs to pay for. You might pay a $25 copay, or fixed amount for a doctor visit. You also pay a share of medical costs called coinsurance, like 40% of a hospital bill, while your plan pays the rest.

- Deductibles, copayments and coinsurance add up to an out-of-pocket maximum, or the most you’ll pay in a year. Once you get there, your plan pays 100% for covered services.

Consider how much you might need:

- How much did you spend last year? Did you pay more out of pocket than you expected?

- Do you have a chronic condition that requires regular doctor visits, medications or treatments?

- Are you planning any major costs, like surgery or pregnancy?

- Do you take monthly medications? Are any of them expensive? What is the yearly cost? Check to see if the plans you consider cover those medications. (Check Community Health Options list here.)

- Are your preferred doctors, hospitals and specialists in the plan’s network? (Check Community Health Options here. Note that this list will be updated on Jan. 1, 2026. Contact Member Services with specific questions.)

- Do you need dental and vision coverage? Do you or your dependents wear glasses or contacts?

- What would it cost you for an unexpected trip to an Emergency Department, serious injury or illness?

Factor in non-medical considerations. If you choose a plan with a high deductible, a Health Savings Account (HSA) could allow you to lower costs saving some of your income in a tax-free account used to pay for qualified medical expenses. That's especially true now, with new federal rules that have made all Marketplace Bronze plans eligible for an HSA. Consult with your broker for which options work best for you.

Want to talk with someone at Community Health Options about which plan to choose? Schedule a call here. If you have questions about your current plan or benefits, please call our Maine-based Member Services team at (855) 624-6463 or email us and we’ll get back to you.

Follow @communityhealthoptions on TikTok for quick tips and tricks on how to buy and use a health plan. And don’t forget to follow Community Health Options on LinkedIn, Facebook or Instagram.

Related Blog Posts

Beyond the red tape: How Prior Approval helps get the right care

We get it. You have a nagging pain in your back that just won’t go away, so you go see your doctor, who sends you for an X-ray. Unfortunately, the X-ray doesn’t show a thing, so the next step might be a CT-scan or even an MRI. You may even have to see a specialist depending on the test results.

Hey, guys: Your future self will thank you for getting a check up

Men: This is for you. We’re guessing you think you live a healthy life. You eat well. You’re active. And you feel just fine. But you might be missing out on doing a bit more to take care of yourself.

Need surgery or a medical procedure? How to know what you'll pay

Understanding a few key things about how your health plan works and knowing how to shop around for healthcare services will make it much easier for you to avoid sticker shock and give you confidence to know your costs before you go.